Please click here to download the Prism as PDF.

In the recent case of Vistra ITCL (India) Limited & Ors. v. Mr. Dinkar Venkatasubramanian & Anr.[1], the Supreme Court re-affirmed the legal position that persons who are merely beneficiaries of security by a corporate debtor do not qualify as financial creditors in the corporate insolvency resolution process (“CIRP”) of the corporate debtor. However, the Supreme Court also held that a resolution plan cannot dilute the security interest provided by the corporate debtor in favour of such beneficiaries.

Brief Facts

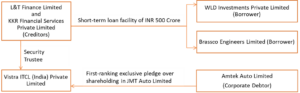

Please find below a diagrammatic structure of the lending transaction derived based on the facts set out in the order of the Supreme Court:

- L&T Finance Limited and KKR India Financial Services Private Limited (collectively, the “Creditors”) had provided a short-term loan facility of INR 500,00,00,000 (Indian Rupees five hundred crore) (“Facility”) to Brassco Engineers Limited and WLD Investments Private Limited (collectively, the “Borrowers”). The Borrowers were group companies of Amtek Auto Limited (“Corporate Debtor” / “Amtek”). The Facility was provided to the Borrowers for the ultimate end use of Amtek.

- Vstra ITCL (India) Private Limited (“Vistra”) was appointed as the security trustee of the Creditors. Amtek created a first-ranking exclusive pledge in favour of Vistra being the security trustee for the Creditors over 66.67% of its shareholding in JMT Auto Limited to secure the Facility availed by the Borrowers (“Pledge”).

- In 2017, the CIRP of Amtek was initiated under the provisions of the Insolvency and Bankruptcy Code, 2016 (“IBC”). Vistra had filed a claim in the CIRP as the secured financial creditor of Amtek, but the same was rejected by the resolution professional (“RP”).

- During the CIRP, in 2018, a resolution plan submitted by Liberty House Group (“LHG”) was approved by the committee of creditors (“CoC”) of the Corporate Debtor as well as by the National Company Law Tribunal, Chandigarh (“NCLT”). However, LHG defaulted in implementing its resolution plan, and the NCLT restored the CoC of Amtek and fresh bids were invited by the RP.

- In 2020, the CoC approved a resolution plan submitted by Deccan Value Investors (“DVI”) and the RP filed an application before the NCLT seeking its approval for DVI’s resolution plan. DVI’s resolution plan negated the Pledge.

- Meanwhile, Vistra and the Creditors filed an application before the NCLT (“Application”) seeking that the RP be directed to include Vistra in the CoC as a secured financial creditor of the Corporate Debtor as they were beneficiaries of the Pledge created by Amtek. The NCLT dismissed the Application and approved the resolution plan of DVI.

- On an appeal filed by Vistra and the Creditors before the National Company Law Appellate Tribunal (“NCLAT”) against the dismissal of the Application by the NCLT, the NCLAT upheld the order of the NCLT and made the following observations:

- Vistra and the Creditors had not challenged the rejection by the RP of Vistra’s claim as the secured financial creditor of Amtek in 2017 after which LHG’s resolution plan was approved, and therefore, it was not open for Vistra to raise this issue later in 2020; and

- Amtek did not owe any financial debt to Vistra as the creation of Pledge did not amount to the grant of any guarantee or indemnity by Amtek to the Creditors.

- Aggrieved by the decision of the NCLAT, Vistra and the Creditors (collectively, the “Appellants”) preferred an appeal before the Supreme Court.

Issues

The Supreme Court was faced with the following issues:

- Whether the challenge raised in the Application against the rejection by the RP of Vistra’s claim as the secured financial creditor of Amtek was hit by delay and laches.

- Whether Vistra is a financial creditor of Amtek in light of the fact that Amtek was the ultimate beneficiary of the Facility.

- Whether the resolution plan of DVI approved by the CoC can dilute, negate or override the Pledge.

Key Arguments by the Parties

Contentions of the Appellants:

The Appellants made the following key submissions before the Supreme Court:

- The Appellants had not challenged the rejection by RP of Vistra’s claim as the secured financial creditor of Amtek because the erstwhile resolution plan of LHG had duly recognized and preserved the Pledge. Nevertheless, the IBC does not prescribe any limitation period for objecting to the categorization of a creditor in a wrongful category.

- The concept of limitation is connected with the principle of cause of action. The rejection of Vistra’s claim gives rise to a continuous cause of action as the RP, the CoC, the resolution applicant and the NCLT are all required to consider the correct categorization of the creditors of a corporate debtor. Therefore, the Application cannot be said to be hit by delay and laches.

- Further, the Appellants had challenged the non-inclusion of Vistra’s claim before the CoC, 5 (five) months prior to the approval of DVI’s resolution plan. Therefore, the question of delay by the Appellants in raising the challenge did not arise, especially when the CIRP of Amtek itself had been continuing for 3 (three) years and had crossed the timeline of 330 (three hundred thirty) days prescribed under the IBC.

- There is a creditor-debtor relationship between the Appellants and Amtek as the Facility was availed by the Borrowers from the Appellants for the end use of Amtek itself, in particular, to standardize Amtek’s loan account with banks.

- DVI’s resolution plan does not meet the requirements of IBC as it extinguishes the Pledge, leaving Vistra, a secured creditor of Amtek, remediless and worse off than its dissenting financial creditors and operational creditors.

Contentions of the RP and the CoC:

The RP and the CoC made the following key submissions before the Supreme Court:

- The Appellants had not objected to the erstwhile resolution plan of LHG, and thereby, to Vistra’s non-classification as a financial creditor of Amtek. Accordingly, the challenge raised by them at a later point cannot be accepted on account of laches and acquiescence.

- Amtek has merely provided a third-party security to Vistra (through the Pledge) in lieu of the Facility. Therefore, Vistra cannot be considered to be a financial creditor of Amtek in view of the judgments of the Supreme Court in Anuj Jain Interim Resolution Professional for Jaypee Infratech Limited v. Axis Bank Limited (“Anuj Jain Case”)[2] and Phoenix ARC Private Limited v. Ketulbhai Ramubhai Patel (“Phoenix ARC Case”)[3].

Analysis and Findings

After considering the submissions of the parties, the Supreme Court made the following observations:

Issue 1. Delay and Laches:

The contention of the RP that the Application is hit by delay and laches as the Appellants failed to object to the erstwhile resolution plan of LHG was not accepted as LHG’s plan did not affect the rights or interests of Vistra as the secured creditor of Amtek in respect of the Pledge.

Issue 2. Status of the Creditors and the Financial Creditors of Amtek:

Even though Amtek was the ultimate beneficiary of the Facility, the liability to repay the Facility was that of the Borrowers and not Amtek. Further, the liability of Amtek towards the Creditors was restricted to the extent of the Pledge. Therefore, in light of the Anuj Jain case and the Phoenix ARC Case, the Supreme Court held that Vistra was not a financial creditor but merely a secured creditor of Amtek.

Issue 3. Negation of Pledge:

- The amendment in 2019 to Section 30(2) of the IBC provided various protections to the dissenting financial creditors and the operational creditors of a corporate debtor in terms of the minimum value to be provided to them under a resolution plan. The Supreme Court observed that the main objective of the 2019 amendment was to recognize and protect the interests of the creditors who are outside the purview of the CoC.

- Further, in terms of Section 52 of IBC, a secured creditor in liquidation proceedings has the right to either realize its security interest or relinquish the same to the liquidation estate and become subject to the distribution of liquidation proceeds as per the waterfall mechanism under Section 53 of the IBC.

- However, in the present case, due to the dilution / negation of the Pledge by DVI’s resolution plan, an odd and peculiar situation has been created where Vistra, a secured creditor of Amtek, is being denied the rights of a secured creditor in terms of Section 52 and 53 of the IBC. In addition to this, since Vistra is not being treated as either a financial creditor or an operational creditor of Amtek, it is also being denied the benefit of the 2019 amendment to the IBC.

- In such a situation, there can be 2 (two) recourses to achieve a fair and just solution:

- to treat Vistra as a financial creditor of Amtek; or

- to treat Vistra as a secured creditor of Amtek in terms of Section 52 read with Section 53 of IBC.

- The first option was not viable in the present case as DVI’s resolution plan was already approved without Vistra being a member of the CoC. Further, it would require reconsideration of the Anuj Jain Case and the Phoenix ARC Case. Therefore, the second option had to be availed.

- Consequently, Vistra should be treated as the secured creditor of Amtek and would be entitled to retain the security interest in, and the security proceeds on the sale of, the pledged shares in terms of Section 52 of IBC.

- These directions are being given to ensure that DVI’s resolution plan meets the mandate of the IBC and does not violate the rights of the secured creditor, who cannot be treated worse off / inferior in its claim and rights viz. an operational creditor or a dissenting financial creditor. The Supreme Court also clarified that these directions would not be a ground for DVI to withdraw its resolution plan.

Conclusion

The Supreme Court has upheld the legal position that in case a corporate debtor provides security for the borrowing of a third party, the beneficiaries of such security will not be considered as the financial creditors of the corporate debtor under the provisions of the IBC. In order for them to be treated as financial creditors of the security provider if they want to be a part of the CoC and exercise voting rights in case of the insolvency of such security provider, such third-party beneficiaries of a security would need to also benefit from a guarantee or indemnity for a financial debt from the corporate debtor. Nevertheless, even if such third party beneficiaries are not classified as financial creditors, this judgment has provided a safety net to them by preserving their security interest against any dilution or negation by an approved resolution plan in the CIRP of third-party security provider.

However, the judgment does not provide any clarity or guidance on the value that needs to be provided by a resolution applicant to the security beneficiaries. It appears to leave the determination of such value up to a negotiation between the security beneficiaries and the resolution applicant.

This Prism has been prepared by:

|

Aashit Shah |

Malika Tiwari |

For more details, please contact [email protected]

[1] Civil Appeal No. 3606 of 2020

[2] (2020) 8 SCC 401

[3] (2021) 2 SCC 799